Banks are under more pressure than ever to deliver always on, friction free, resilient payments experiences. Yet many financial institutions still rely on payments platforms originally built to support an entirely different era of banking.

Even if those systems are technically still functioning, they may be approaching what’s known as their effective end of life (EOL) — the point at which the platform can no longer keep pace with business, regulatory, operational, or customer expectations.

Understanding when you’ve reached that threshold — and what to do next — is critical for protecting your payments business and preparing for the future.

1. The Real Question: Is the Platform Supporting the Business You Need Today and Tomorrow?

1. The Real Question: Is the Platform Supporting the Business You Need Today and Tomorrow?

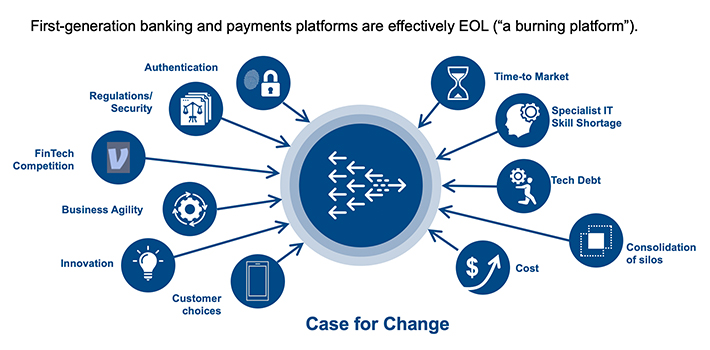

Most banks don’t need another reminder that legacy systems are old. What they do need is clarity on how to recognize when a platform’s limitations are actively constraining growth, innovation, and operational stability. Key signs your platform may be hitting its effective EOL include:

- Increasing difficulty keeping up with regulatory and scheme changes. If updates require long lead times, expensive custom work, or risky manual interventions, the platform may no longer be fit for a rapidly evolving payments ecosystem.

- Rising operational incidents or outages. Performance bottlenecks, latency during peak periods, and growing downtime windows signal that the underlying architecture can’t scale with demand.

- Heavy reliance on individual experts or tribal knowledge. If only a few system specialists can support or troubleshoot the platform, your operational risk skyrockets.

- Roadblocks to launching new payment types or channels. When rolling out a new capability takes months instead of weeks, the technology is actively restricting your competitive position.

- High cost of change. Legacy platforms often require custom coding, complicated regression testing, and lengthy deployment cycles — all of which drive up cost and slow down transformation.

2. Understanding the True Cost of “Waiting Just a Bit Longer”

Banks often delay modernization because:

- The system is “still working”

- Change feels risky

- Budgets prioritize more visible initiatives

- Stakeholders underestimate the long term impact

But the cost of keeping a platform past its effective EOL typically exceeds the cost of modernizing. Risks grow. Change becomes harder. Talent becomes scarcer. Technical debt compounds. And most importantly, the bank’s ability to compete in payments steadily erodes. Modernization is no longer a technology decision — it’s a business continuity decision.

3. What Banks Should Look for in a Next Generation Payments Platform

When evaluating the future of your payments environment, shift the focus from “feature checklists” to capabilities that sustain long term resilience and growth.

- Cloud-native, microservices architecture. Supports elastic scaling and faster innovation cycles.

- API driven interoperability. Allows you to quickly integrate new channels, partners, and rails without breaking existing systems.

- Real time processing support. Essential for instant payments, fraud decisioning, and deliverying on customer expectations.

- Strong monitoring, analytics, and observability. Provides transparency and proactive incident prevention.

- Support for hybrid environments during transition and upgrades. Let’s you modernize at your own pace without disrupting service.

- Reduced dependency on proprietary expertise. The platform should be supported by modern skills, documentation, and tooling, including AI where it can accelerate efficiences and decision making.

4. A Modernization Path That Minimizes Disruption

Banks don’t need to replace everything at once. Many choose to:

- Introduce a modern transaction layer

- Migrate channels and payments incrementally

- Reduce risk by running legacy and new systems in parallel

- Shift gradually to real time and cloud enabled capabilities

A layered, modular modernization strategy gives banks control, flexibility, and lower risk — and avoids the “big bang” cutovers that institutions understandably want to avoid.

Let Vynamic® Transaction Middleware Accelerate the Journey

While this blog focuses on what banks themselves need to understand, evaluate, and control, choosing the right payments modernization platform can make the journey significantly easier.

Vynamic® Transaction Middleware is designed to sit at the center of a bank’s transaction processing environment, providing a modern, modular, cloud-native foundation that simplifies migration, reduces operational risk, and enables new payments capabilities without forcing a full scale rip and replace.

It becomes a strategic enabler — a quiet hero behind the scenes — so banks can modernize on their terms and accelerate their payments transformation with confidence.

Join the growing list of over 80 leading FIs around the world who are putting their trust in the new world of payments with Diebold Nixdorf. Contact us to see how Vynamic Transaction Middleware supports your transitions.

.jpg?w=361&h=209&mode=crop&hash=CCDF44BFCA12EF070E01ACA16598F57A)