Retail banking executives across the globe face a familiar but intensifying dilemma: how to deliver greater operational efficiency while meeting rising customer expectations in an increasingly crowded and competitive market.

Margins remain under pressure, operating complexity continues to grow, and consumers—empowered by digital choice—are more willing than ever to move funds, open secondary accounts, or quietly shift their primary banking relationships elsewhere.

In this environment, the debate around build versus outsource has moved beyond cost savings alone. For many financial institutions, outsourcing and managed services are evolving into a strategic lever—one that enables scale, resilience and consistency while freeing internal teams to focus on differentiation and growth.

Consumers are raising the bar—and lowering their loyalty

Today’s retail banking customers expect frictionless, always on service across channels, rapid response times, and personalized experiences that feel relevant to their daily lives. Importantly, these expectations are shaped not only by other banks but also by digital brands in retail, travel, and technology. When banking experiences fall short, consumers no longer protest loudly—they simply add another provider and reallocate their activity.

This behavior has profound operational implications. Banks must deliver high service quality across millions of interactions every day, often at lower unit cost and across more channels than ever before. Achieving this solely with in house resources is increasingly difficult, particularly when skilled talent is scarce, and operating costs remain high.

Efficiency today is operational excellence, not austerity

For years, “efficiency” in banking was synonymous with cost-cutting—branch closures, headcount reductions, and investment restraint. Today, that definition has changed. Efficiency is now about doing more with less friction, combining automation, modern platforms, and highly standardized operations to deliver faster, better outcomes for customers.

This shift explains why outsourcing is no longer limited to infrastructure or narrow IT functions. Increasingly, banks are extending managed service models into end to end operations, including transaction processing, service desk activities, monitoring, incident handling, and even certain customer support functions.

Rather than hollowing out capabilities, well designed outsourcing can industrialize them—bringing repeatability, 24/7 availability, and continuous improvement that is difficult to replicate internally at scale.

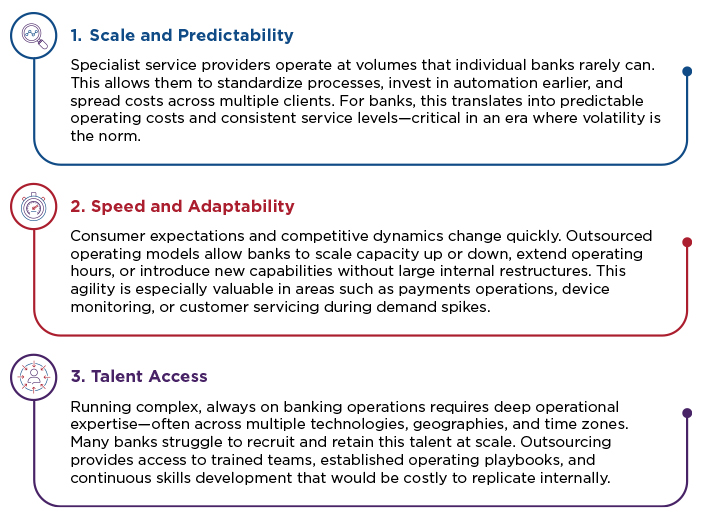

Why outsourcing is gaining momentum

There are three core reasons outsourcing and managed services are becoming more attractive to retail banks worldwide

Beyond platforms: running the bank, every day

While much attention has focused on outsourcing technology platforms, the greater impact often comes from outsourcing day to day operations.

Consider a mid sized retail bank operating across several countries. Internally, it maintained separate teams for transaction monitoring, fraud alerts, customer service escalation, and IT incident response—resulting in handoffs, delays, and inconsistent customer outcomes. By consolidating these activities into an integrated managed services model, the bank was able to align operational workflows end to end. Resolution times improved, service availability extended, and customer complaints fell—even as operating costs declined.

Another example comes from self service channel operations. Many banks still manage ATM, kiosk, or branch technology support internally, with local staff handling monitoring, dispatch, and issue resolution. Institutions that have moved these responsibilities to managed operations providers often see improvements in uptime and predictability. Because providers manage thousands of devices across clients, they can apply advanced analytics, proactive maintenance, and standardized response processes—reducing outages that customers immediately notice.

These examples highlight a crucial point: customers do not experience organizational charts. They experience outcomes. Outsourcing operational execution can enhance those outcomes when it is designed around service quality rather than simply cost reduction.

Addressing the fear of losing control

One of the most common objections to outsourcing core operations is fear of losing control or accountability. In practice, leading banks address this not by retaining execution internally, but by strengthening ownership of outcomes, governance, and performance management.

Successful outsourcing relationships are characterized by:

In this model, banks do not abdicate responsibility; they shift their focus from doing to directing. This often results in better transparency and stronger performance discipline than fragmented in house delivery models.

A pragmatic answer to the “promiscuous consumer” challenge

As customers maintain multiple banking relationships, differentiation becomes less about individual features and more about consistency and reliability. Banks that struggle operationally lose credibility quickly, even if their products are competitive.

Outsourcing helps address this challenge by stabilizing the operational core—ensuring that payments clear on time, service inquiries are handled efficiently, and channels remain available. This stability allows internal teams to focus on what truly differentiates the bank: product innovation, customer engagement, financial advice, and brand trust.

Importantly, outsourcing also enables faster improvement cycles. When performance data, automation, and service optimization are built into the operating model, banks can adapt more quickly to shifting expectations—something that purely in house organizations often find difficult.

A strategic choice, not a tactical shortcut

Outsourcing is no longer a tactical decision about cost relief. It is a strategic choice about how retail banks operate in a world of demanding, mobile, and digitally empowered customers.

The most successful institutions are not asking whether outsourcing is good or bad. They are asking:

For many banks, the answer points clearly toward managed services—across both technology platforms and day to day operations—as a foundation for sustainable efficiency and competitive resilience.

Diebold Nixdorf brings expertise in exactly this space – our Branch Automation Solutions integrate self-service, branch and digital capabilities to help financial institutions operate more efficiently and serve their customers more effectively, at scale. If that is a journey your institution is ready to take, we would be glad to explore it together.