For decades, payment transactions largely followed a familiar pattern: a physical card paired with a PIN to authenticate, authorize, and settle a transaction. While effective, this card centric model created dependencies that shaped how financial institutions designed their processes and how consumers interacted with their banks.

Today, that status quo is being upended. New payment methods, diverse digital tokens, and flexible authentication options are accelerating into mainstream use—breaking open possibilities that move far beyond the plastic card. These emerging experiences give consumers more choice and remove long standing frictions built into traditional payment flows.

A New Era of Authentication Flexibility

A New Era of Authentication Flexibility

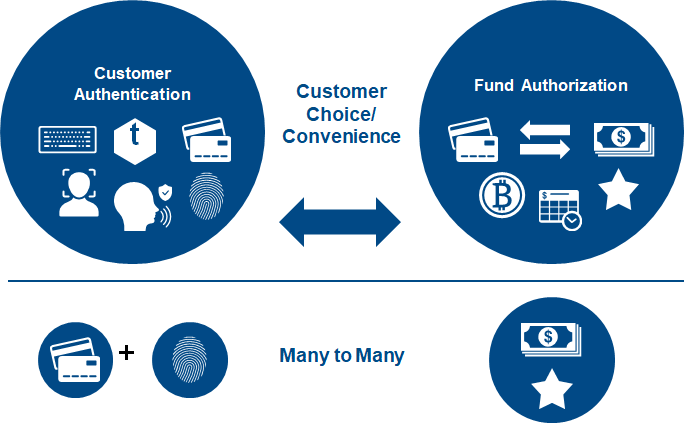

Authenticating a consumer and validating the legitimacy of a transaction remain essential steps. But the ways to accomplish those tasks have multiplied.

Consumers now routinely use:

- Passwords to access online platforms

- Biometrics to open mobile apps and digital wallets

- Tokenization across a growing number of digital services

This shift puts consumers in control — allowing them to “do it their way” regardless of what’s happening behind the scenes. But it also disrupts the existing linear payment process. To stay competitive, financial institutions must now support multiple authentication technologies, encapsulate services, and flexibly combine functions to create best in breed experiences.

Future proofing authentication is no longer optional; it’s foundational to meeting evolving customer expectations.

Decoupling Authentication from Authorization

One of the most powerful changes reshaping the payment landscape is the ability to unbundle the authorization step from authentication. Traditionally, both occurred together on card network rails. Separating them allows financial institutions to:

- Use diverse payment rails beyond traditional card networks

- Reduce dependency on global card schemes

- Support real-time, instant, and split-payment models

- Introduce alternative funding sources such as BNPL, loyalty points, or crypto assets

This decoupling opens the door to more efficient, resilient, and flexible payment ecosystems — and dramatically expands how consumers can fund transactions.

Why This Matters Now

The acceleration of digital payments, the demand for interoperability, and shifting consumer expectations make this the moment for financial institutions to break the payments status quo.

Modernizing the process unlocks:

- Better customer experiences through frictionless, choice driven interactions

- Stronger loyalty as consumers gains more control over how they authenticate and transact

- New revenue opportunities tied to emerging payment instruments and alternative rails

- Operational agility to adapt as new technologies and regulations emerge

To fully realize these opportunities, payments modernization must focus not only on new technology—but on rebuilding the payment journey to be channel agnostic, authentication flexible, and funding agnostic.

The Bottom Line

As financial institutions push beyond legacy limitations and pursue real time, flexible, and frictionless payment experiences, the need for a modern foundation becomes undeniable. Breaking the status quo isn’t just about introducing new payment methods — it’s about redesigning the transaction flow so authentication, funding, and channel experiences can evolve independently and continuously. This is exactly where

Vynamic® Transaction Middleware becomes transformational.

Unlike traditional payment architectures or single purpose software, Vynamic Transaction Middleware serves as the

shared core technology that underpins Diebold Nixdorf’s entire Vynamic software ecosystem. It provides the reusable, cloud native, microservices based components that enable banks and retailers to build, adapt, and scale transaction capabilities across channels without ripping out existing investments.

By treating essential capabilities like authentication, orchestration, routing, monitoring, and security as modular building blocks, Vynamic Transaction Middleware allows institutions to evolve quickly, add new payment types, support instant and account to account rails, or redesign customer journeys — all while maintaining stability and compliance. It delivers the harmonization, speed, resilience, and differentiation that modern payments demand.

For organizations ready to exit the constraints of siloed card centric processes, Vynamic Transaction Middleware provides the strategic path forward. It doesn’t replace the innovation happening across payments — it accelerates it.

How can banks support multiple payment rails without disrupting existing systems?

Contact us today to learn how banks are modernizing payments.