The movement of money has never been faster—or more complex. Today, U.S. credit card networks process nearly 1,781 transactions every second, and globally, that figure exceeds 25,091 transactions per second.

This acceleration is driven by the continued rise of digital commerce, contactless payments, and always connected consumers who expect speed, accuracy, and convenience at all times.

In Visa’s case alone, the network processed

257.5 billion transactions in FY2025, up sharply from 233.8 billion the prior year. underscoring both scale and growth.

For financial institutions (FIs), this speed and scale have reshaped expectations: always-on availability, instant authentication, real-time fraud checks, consistent policy enforcement, and the ability to deploy new customer experiences without operational disruption.

Yet many institutions still depend on

legacy monolithic systems built decades ago— long before real time, omnichannel banking became the global standard. These systems cannot keep up with modern transaction volumes, compliance expectations, or customer experience demands.

The Limits of Legacy Architectures

Most legacy payment hubs were engineered in the 1980s and 1990s, when systems were expensive, static, and designed for predictable batch-based workloads. They center authentication around card-and-PIN, and rely on large, tightly coupled executables that cannot easily scale or evolve.

When a monolith handles authentication, for example, it’s not just executing one routine—it may run dozens of interdependent processes in a fixed sequence. That structure inherently creates:

- Single points of failure

- Bottlenecks during peak events

- Idle capacity during low-volume hours

- Limited ability to roll out new features quickly

Even though transaction loads now swing drastically throughout the day—from quiet midweek periods to high traffic events such as holiday shopping—the monolith forces institutions to maintain large, pre-provisioned environments that sit idle much of the time.

And with payment preferences shifting rapidly—contactless now drives

50%+ of global in person payments, and credit cards still account for

31% of all U.S. payment transactions—institutions can no longer afford slow, rigid infrastructures.

Why Modernization Matters Now

Consumers increasingly expect:

- Instant authentication across channels

- Seamless e-commerce checkouts

- Built in fraud protection

- Biometric or token-based verification

- Real-time balance updates

- Personalized limits and controls

Behind the scenes, this requires tremendous processing power, dynamic routing, scalable compute, and modular business logic. The rising complexity and velocity of transactions—combined with growing regulatory scrutiny—make modernization a competitive and operational necessity.

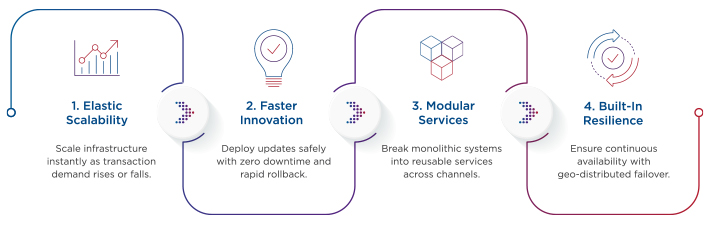

Microservices: Building for Scale, Resilience and Agility

Microservices: Building for Scale, Resilience and Agility

Modern, cloud native payment systems built on microservices eliminate the constraints of legacy systems and enable true real time, high volume processing.

1. Elastic Scalability (Up and Down). Instead of maintaining oversized servers year round, microservices run in lightweight containers that automatically scale to accommodate demand. During high volume events, new service instances spin up instantly; during lulls, resources scale down—improving efficiency and optimizing costs.

This is critical when networks like Visa are processing hundreds of millions of transactions per day.

2. Faster, Safer Innovation. Microservices allow teams to deploy updates or new services using blue/green models—introducing changes with zero downtime and quick rollback if needed.

Examples include:

- Adding new biometric authentication without touching core processing code

- Updating fraud models in isolation

- Rolling out compliance changes instantly across channels

- Adjusting risk and transaction limit rules through configuration rather than code

3. Breaking Down the Monolith. Large functional areas — authentication, limits management, security — are decomposed into reusable, centralized services.

This ensures consistent policy enforcement across:

- ATMs

- Mobile apps

- Teller platforms

- Digital banking channels

When policies change, updates can be applied enterprise wide rather than navigating legacy code pathways in multiple systems.

4. Multi-active Resiliency and Geo Redundancy. Modern microservice architectures support geo distributed failover, real time scaling, and multi-active redundancy, ensuring continuous service availability even during failures or regional outages.

This directly supports consumer expectations of uninterrupted, 24/7/365 access.

Future-Proofing the Payments Ecosystem

As the number of credit cards in circulation surpasses 800 million in the U.S. alone and digital commerce continues its rapid expansion, FIs must operate with infrastructure capable of:

- Real-time decisioning

- High volume API throughput

- Dynamic routing and orchestration

- Continuous integration & delivery

- Seamless fintech and open banking integration

Diebold Nixdorf’s

Vynamic® Transaction Middleware gives institutions a modular, cloud ready foundation to modernize without disruption — unifying ATM, mobile, branch, and back office payment services in a single intelligent layer.

Is Your Organization Ready to Evolve?

The payments landscape is accelerating faster than ever. Transaction volumes are increasing, consumer expectations are higher, and competitive pressures are intensifying. Only institutions built on flexible, cloud native, microservice driven systems will keep up.

Payments modernization isn’t an upgrade — it’s a strategic shift.

It unlocks the speed, resilience, and scalability needed to thrive in a real time world.

Is your organization ready to future-proof your banking ecosystem?

Let’s discuss how

Vynamic Transaction Middleware can help you evolve your payments system.

.jpg?w=361&h=209&mode=crop&hash=3A4C2EA276F8BDCBE3B11753280610FE)